Elliot TurnerPosted on Friday, March 30, 2012 at 9:57AM

A Template for Understanding: How the Economic Machine Works... (Bridgewater) -- This is a MUST READ, and I mean that to the fullest. Ray Dalio and Bridgewater lay out a more complete, robust and accurate assessment for how an economy works than anything we see in the financial presses. Plus the write-up is concise and written in layman's terms so that anyone and everyone can extract real value. Reading this report should be a prerequisite for ANY candidate who runs for office, maybe then our economic rhetoric would be a bit more complex, but way more rational? One can dream!

Google Cloud: Coming Soon to Robots Near You (Seeking Alpha) -- To date, the robotics story has primarily been hardware driven, based on innovation in mimicking human movements and/or actions based on necessity. Now the rapid advance in software is adding a whole new dimension and setting the stage for the dawn of widespread adoption of robotics. While on the topic, check out this awesome video of a robot that can jump over 30 feet if need be!

World's Changed Man, World's Changed-China Edition (Financial Times) -- This is from earlier in March, but still just as relevant. Throughout the month, each market downtick was more a reflection of concerns over China than Europe. That's quite the change from this past summer. What are the consequences? Well one might be the end of the big commodity bull that's lasted over a decade. Can the commodity bull persist if China slows? Does this bode as a positive, or a negative for the US? These have been the questions that I spent the majority of my attention on this past week. I should have some charts and analysis within the next two weeks.

Insane in the Membrane (Outside Magazine via Readability) -- This is a fascinating long read on the history of Gore-Tex and the state of the waterproof, breathable fabric market. There is an intense battle being waged for market dominance that includes some interesting twists and turns.

How the Natural Gas Craze Will Impact Clean Energy (GigaOM) -- This is an issue I have spent quite a bit of time contemplating myself. Is natural gas a transitory or enduring shift in terms of efficiency, cost and environmental cleanliness? If so, what are the consequences for clean energy on each of those variables as well? We seem to be at a big inflection point in the adoption of both. Is this an "either or" proposition, or can both succeed? There are way more questions than answers right now, and in these answers lies considerable opportunity.

Why Minsky Matters (EconoMonitor) -- In my book, Minsky is the most important economist today. Yet, there's a bit of a debate going no amongst the new age Keynesians as to how exactly Minsky is relevant. Here is L. Wrandall Wray's analysis as to why Minsky is so damn important. It's slightly wonky, but a must read for anyone interested in macroeconomics.

Praise is Fleeting, but Brickbats We Recall (NY Times) -- Really fascinating psychological analysis of how the mind processes negatives in contrast to positives. We tend to recall negatives more frequently and with more clarity and this has to do with how the brain works. Understanding psychology generally speaking is very important in improving as an investor.

I usually close with one of my nature pictures, but today I will leave you all with this awesome video presentation taking advantage of the power of the iPad:

Elliot TurnerPosted on Monday, March 26, 2012 at 7:28PM

With equity markets breaking out to multi-year highs, amidst a persistent spate of negativity, there are all kinds of stories designed to scare people into thinking there is something sinister behind the rally. Some argue that without Apple, the S&P 500 would be going nowhere, some argue that profit margins are too high and must regress, while others argue that the cyclically adjusted P/E (CAPE) remains elevated and inconsistent with a longer-term bottom). All of these arguments have some merit, but none of them measure a key point: today’s S&P 500 is not yesterday’s S&P 500.

What do I mean by this? Well quite simply, there is some serious Darwinism going on in the indices, with the outcome being that survival of the fittest has a strong upward bias. Since the market peaked in October of 2007, exactly 100 companies have been added, and 100 removed from the S&P, with the vast majority of the change having happened during the 2008-09 collapse. I don’t have the long-term data, but I would surmise a guess that this was the period of the highest turnover in our most prominent benchmark index EVER. If anyone has the data necessary to confirm this, I would greatly appreciate it. Regardless, I think it’s safe to say that at the very least, over these last few years we have witnessed one of the largest shakeups in the constituent holdings of the S&P since the Index’s inception.

This is consequential for many reasons. One particularly important reason, and the inspiration behind my digging into the numbers is the fact that while reading numerous comparisons of the S&P 500 pre and post-2007, not a single analysis I have seen has mentioned or attempted to dig into the composition of the index. Meanwhile every day I read something that tries to assert Apple is skewing the index. After looking at the data, it’s become clear that while Apple is a large force, the turnover in the constituent holdings has had a much bigger impact. Just from the turnover alone, the S&P has been tilted away from financials and old sluggish companies with little to no growth, towards technology and innovative, young companies with rapid expansion.

Out of the 100 companies removed from the S&P 500, 20 were financials that either went bust, were bought out while in distress, or their market caps shrunk so much they were no longer relevant. Another 7 companies either went bankrupt, or were near bankrupt due to their exposure to the debt crisis, or the rapid disruption of their business model during the crash.

Here’s a selective list of some notable removals from the S&P 500 since October, 2007 (this list is not comprehensive, but rather just some notable departures):

Circuit Cities

Ambac Financial Group

Countrywide Financial Corp.

Federal Home Loan Mortgage Corp (aka Freddie Mac)

Federal National Mortgage Association (aka Fannie Mae)

Lehman Brothers

Washington Mutual

Merrill Lynch

General Motors

CIT Group

MBIA

KB Home

RadioShack

Eastman Kodak

The New York Times

Some Notable Additions (again, not a comprehensive list):

Intuitive Surgical

MasterCard

Salesforce.com

Life Technologies

Red Hat

Priceline.com

Visa

Ross Stores

Urban Outfitters

Berkshire Hathaway

TripAdvisor

Chipotle

Blackrock

F5 Networks

Netflix

Note how the list of removals is populated with many very old companies, with a heavy concentration of financials and other legacy US businesses that have either gone, are near, or were on the brink of bankruptcy. Meanwhile, the list of newcomers includes many of the hottest “new” economy companies that are core components of today’s thriving digital age. Berkshire Hathaway stands out like a sore thumb on the list of newbies, as the company entered the S&P 500 upon completion of its acquisition of Burlington Northern and splitting the “B” shares. Berkshire “replaced” BNI in the index, thus finally bringing one of America’s largest, most profitable businesses into the composite that is designed to represent American business. This is a big change, as Berkshire is now one of index’ 10 largest holdings.

This all has a meaningful impact on the intrinsic metrics of the S&P, including earnings, growth, and most importantly, performance. Priceline is the best performer on the list of newcomers, and it alone is up 779% since the market bottomed in March of 2009. That is pretty remarkable compared to Lehman Brothers, which only this month “emerged” from bankruptcy as a nearly worthless entity for equity holders.

Not that these facts alone mean the market should be moving higher, but it is very important to contextualize what we mean when we say “the S&P 500 is making new multi-year highs” and conduct any analysis that relies on index-wide metrics. Had these changes not transpired, one can reasonably guess that the S&P 500 would be closer to 1,000 than 1,400 today. And that is a good thing! Evolution is a powerful, natural force that drives things forward and helps to overcome yesterday’s vulnerabilities. It is progress, hence it is a more valuable total index.

Elliot TurnerPosted on Friday, March 23, 2012 at 10:53AM

It's Friday again, that means it's time for more links for thought!

Jonah Lehrer and the New Science of Creativity (Why We Reason) -- If you read one article from this post, this should probably be it. It's points are so widely applicable and relevant to everyone. The post takes is a book review on Jonah Lehrer's new book called Imagine: How Creativity Worksand takes look at the creative science behind Bob Dylan plugging.

Please Stop Apologizing (NY Times) -- Bill Maher tells everyone to chill out and stop apologizing. He also proposes that we "make this Sunday the National Day of No Outrage. One day a year when you will not find some tiny thing someone did or said and pretend you can barely continue functioning until they apologize." Great points from Maher about how hyper-sensitivity has been taken way too far in general, and has simply become a distraction from the real, important questions in life.

The Man Who Broke Atlantic City (The Atlantic) -- Awesome article on Don Johnson, the man who won $6 million playing blackjack in just one night, and over $15 million in a short time. There are many lessons to take from this article, particularly from an investment perspective. Any investor should do as Johnson did, and seek to stack the odds in your favor, while those same investors should never do what the casino did in desperately seeking a way to make a buck.

5 Things that Surprised Me About A Career on Wall Street (Ritholtz) -- As a lawyer turned investor, this really struck a chord with me. Barry Ritholtz too comes from the same background, and he takes a stab here at some of the real shocks of entering the investment world. Point #1 in particular should hit EVERYONE on Wall Street real hard, because it is just so damn true: "Surprisingly few people rolled up their sleeves and thought deeply about why things in market are the way the are."

A Stock is a Business (Oddball Stocks) -- This is something I say and will continue to say often, "a stock is a business." It is not a line on a chart, it is not a spreadsheet of ratios, it is a real, vibrant business. Oddball Stocks takes a good look here at why that's an important point and how it impacts investment analysis.

Elliot TurnerPosted on Tuesday, March 20, 2012 at 3:45PM

Want to invest in one of the best, most innovative startups in the world with taking none of the risk associated with a startup, and more potential upside than many of the most popularly watched private market web names like Facebook? Look no further than the strongest brand hiding behind the Google name: YouTube. YouTube is turning into a huge business, and were it a standalone start-up, the company would easily be one of the most valuable Internet companies and one of the most hyped. Instead we hear little about YouTube’s business other than the obligatory question and non-answer answer on each Google quarterly conference call about when/if/how much money YouTube will make.

Today, YouTube seems even more an afterthought in the narrative about Google the company than Android and Google + and I can’t help but find the irony and humor in it all. While everyone is waiting for Google’s true “social” answer, and even Google itself is out there searching (pun intended), YouTube is in fact a social, technology and media behemoth in its own right. After all, it is the place where “going viral” became the thing to do (speaking of which, here’s a cool video with Kevin Alloca, YouTube’s “trends manager” on what actually makes a video go viral).

Facebook is the startup darling of the world, Netflix at times has been the streaming superstar, and Apple is…well…the apple of everyone’s eye. Meanwhile in between watching hours of YouTube videos a day, everyone forgets that a) YouTube has an amazing business model and b) Google is both cheap and sitting on a competitive Trojan Horse. Let me explain.

The Cost of Content

I’m oversimplifying here, but in content, there are the producers, the distributors and the consumers. When anyone talks about content distribution companies, and video in particular, the cost of content is important in determining the bottom-line profit. The true advantage of streaming video is that on a relatively small fixed cost base, a distributor can reach every web-connected person on Earth. In an ideal world, that sounds like a simple and great business, but the content producers have only been willing to engage the distributors with largely one-sided terms.

The content producers know full well the value in distributing via the Internet, so they even created their own distribution service—Hulu.com. Netflix has used its DVD business, the company’s cash flow machine, in order to fund content acquisition for its streaming service. As streaming has gotten easier and more popular amongst the masses, many have fled DVDs for streaming, thus forcing Netflix to improve its content mix online. As their early contracts expired, the company found itself having to negotiate in a position of need with the studios, and since then has paid a hefty price.

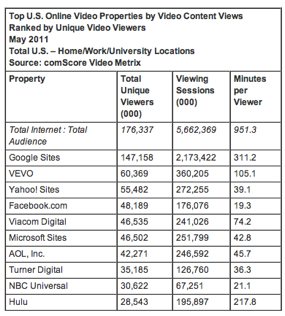

Meanwhile, YouTube just keeps doing its thing. Worldwide, people view 3 billion YouTube videos per day, which for perspective is “the equivalent of nearly half the world’s population watching a YouTube video each day, or every U.S. resident watching at least nine videos a day.” While Netflix and Amazon are out paying (more like begging for the right to pay) for content, YouTube users are willingly uploading 48 hours of content per minute for FREE. Granted not all YouTube content is as desirable as the content others are paying for, but considering how many people watch videos on the site every day, it’s safe to conclude that at every minute YouTube is gaining more valuable content at no expense.

With this recipe, YouTube has become the most watched online video site by a mile (h/t to TechCrunch for the chart):

In the process, YouTube has already become a heavily entrench business with a strong brand name and strong brand loyalty. When people talk about the competition for online video success, particularly in financial circles, the competition pits Netflix against Amazon, with Apple sometimes entering the fray and Google a total afterthought. That needs to stop.

As of today, YouTube has already reached deals with CBS, BBC, Universal Music Group, Sony Music Group, Warner Music Group, the NBA and the Sundance channel, amongst others (contract list from the CrunchBase). Some of these deals were reactionary to growing pressure from content producers at the copyright infringing uploads done by YouTube users, but at the end of the day, these content deals have done a whole lot to enhance the quality of the videos available on YouTube and entrench the site as THE go to platform for video.

Notice a theme with these content deals? Many of the early deals are music-centric. There is no better place on the Web to watch high quality concert video than YouTube, nor is there a better place for an artist to debut their new song via a video (even VEVO uses YouTube), with MTV now a soap-opera-type channel lacking any coherent connection to music. Witness Cee-lo Green’s catchy release of F*ck You with the words literally dancing across a blue projection screen. This was both a powerful and catchy way for Cee-lo to get his song out to the masses, and was a catalyst behind the song’s ascent on the pop charts.

YouTube the Platform

The Cee-lo release provides the perfect segue to YouTube as a platform. YouTube is a disruptive medium in itself, but more interestingly it has become a platform upon which other disruptions are launched. At the same time, YouTube has also become a video platform that is ubiquitous across all viewing platforms. Although a web-page in itself, YouTube is a “channel” (rather app, but what’s the difference these days?) on any web-enabled TV device from designated viewing devices like the Roku or AppleTV to gaming systems like the Xbox. The point is that YouTube has both incredible reach to its audience, and is an innovative vehicle for some of the world’s foremost innovators. Even Apple can’t deny this reality.

In addition to debuting singles on YouTube, there are successful artists who owe their entire careers to the medium. Look no farther than Justin Bieber (geez I promised myself that name would never be typed into this blog…), someone who would never have been “found” had it not been for the site. Bieber isn’t alone. Daniel Tosh has built an incredibly popular show on Comedy Central based entirely off of YouTube videos, and the Young Turks have become serious news pundits from their YouTube show.

Louis CK, a comedian with a strong cult following, used YouTube in an entirely new way by releasing his “Live at the Beacon” directly through the platform. “Lucky” Louis went on to sell this show for $5, with customers able to pay and watch instantly. This is far cheaper than a DVD retails for, and a much easier way to directly connect with an audience. The move was both highly profitable for Louis, and rewarding for his fan base.

When you have a business that works better for all the parties directly involved than the existing business model, you have a powerful force. It’s cheaper for fans, more profitable for the artist, reaches a far wider audience than anything else, and has fewer intermediaries taking a cut. Stuck in the middle is YouTube/Google easily (and happily) collecting its margin. It’s only a matter of time before more artists follow Louis down this path.

And YouTube’s appeal isn’t limited to music, comedy and entertainment. The Khan Academy is using YouTube as platform to disrupt education. While it is a non-profit that produces free, high quality educational content for view via the YouTube platform, let’s not dismiss the fact that the Khan Academy is proving the power of the platform as a way to not only reach those interested in learning, but to fundamentally change the way eager students learn. TED Talks has also used YouTube in a similar manner as a platform to bring informative, educational videos to the masses. We’re only just beginning.

YouTube and the Innovator’s Dilemma

YouTube is following the path of the Innovator’s Dilemma, and all of the dominant market leaders in the sectors impacted by the company are already on high alert (if you haven’t already done so, go read the book now, or for a short-cut read my blog post on it). YouTube has firmly entrenched itself on the low-end of the video-watching marketplace, and I mean this both in terms of Internet video, and video in the broadest possible terms. Further, YouTube has significantly deflated the cost of distribution and consumption, making both effectively free in many contexts for the content producer and the viewer respectively. In doing so, YouTube generates a fairly high margin on its advertising dollars on.

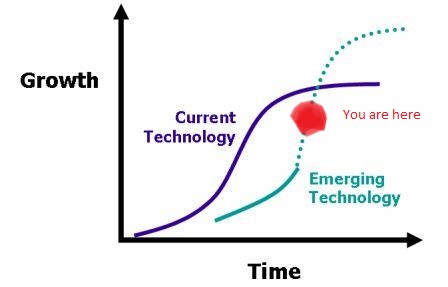

As YouTube has earned more and more money on the “low hanging fruit” (aka the free stuff) they have been able to step up their acquisition of premium, higher quality content. Some of the aforementioned deals are evidence of this. In other words, the company is using its entry level product, which has helped it gain market share, in order to fund its climb higher up the distribution tree. As a result, the company is in the midst of a further pivot up its S-curve (H/T to Your Brand is Showing for the graph).

The current technology is the combination of TV/Cable/Internet that we presently view video on, while the emerging technology is YouTube. In my imprecise opinion, right now YouTube is somewhere around the big red dot that I drew on top of the chart. The company is on its parabolic ascent, but has yet to reach and cross the current technology in its prowess, largely due to the defensive posturing of the existing infrastructure. But that can’t last forever. As the chart indicates, and as is typical with disruptive innovation, YouTube’s day is coming rather quickly. Keep in mind we’re talking about a company and technology barely more than six years old. It was within the past two years that we were introduced to high definition video for streaming, that we were able to watch YouTube video’s on our television, and even more recently, that content was divided into organized channels.

Not long ago, YouTube had a major success in acquiring streaming rights to a premier Indian cricket tournament for live games. Viewership surged far quicker than anticipated, and was more profitable than anyone expected. Soon many of the major sports leagues will have their television contracts expiring, and one can imagine that YouTube will be a player for the rights, especially considering their already strong relationship with leagues like the NBA and NHL. If YouTube were in fact the first to bring mass-streaming of live sporting events to the American masses, they would be the first to truly liberate video viewing from the existing infrastructure and into the digital age. After all, live sports viewership is probably the single largest impediment to would-be chord cutters today (myself included).

YouTube gets this, as is evidenced by what CEO Salar Kamangar recently had to say: (h/t to New Markets Advisors, I strongly recommend reading their write-up on the disruptive power of YouTube as well):

"When you think about the impact cable had, we think we're in a position to have a similar impact for video delivery, like what cable has done with broadcast. In the early '80s, you had three or four networks. Now those three or four networks are responsible for 25 percent of viewership, and the cable networks are responsible for all the rest. Right now, the fraction of traffic that is Web video is small relative to broadcast and cable, but it's growing at a fast rate. What's amazing is that the Web enables you to build a kind of channel that wouldn't have made sense for cable, in the same way cable enabled you to build content that wouldn't have made sense for broadcast. You couldn't have done CNN with the broadcast networks; you couldn't have done MTV with the broadcast networks."

And here’s a great TED talk with Chris Anderson, Editor in Chief of Wired Magazine, on “How YouTube is Driving Innovation”: (obviously an embedded YouTube video)

Putting the Story in Context with the Numbers

Now that I have established a benchmark for how awesome and disruptive YouTube is, the next step is to take a look at the number. If you’ll remember, my initial premise was that one can buy one of the most disruptive, innovative companies today without taking any of the venture capital risk, for free. This requires that I establish two premises: 1) that Google without YouTube is at most, fairly priced, if not downright cheap, and 2) that YouTube as a stand-alone entity would be worth a sum exceeding $10 billion in market cap, and in a range that reaches northward of $20 billion. For that I will have to follow-up with a second post, but I will not leave just yet before beginning the next step of the argument.

Using consensus analyst estimates on revenue for 2012 (courtesy of Business Week), a 10% WACC and 4% perpetual growth, Google has an earnings power value plus growth of $680, that is a 7% premium to this price. YouTube itself accounts for a mere 4% of Google’s in this estimate, and if you removed YouTube’s revenue contribution entirely from Google, the price drops to $653, a 3% premium to today’s price. From this, we can deduce that YouTube represents about $27 per each share of Google, or a total intrinsic value of $8.7 billion.

Before next week’s post on how to value YouTube, I just want to finish off by stating my belief that $8.7 billion is way too cheap for such a valuable web property, especially when companies with lower revenues like LinkedIn and Zynga are trading for near $10 billion, and Facebook is pricing at over $100 billion. In a recent social brand value analysis by BV4, a brand value ratings agency, Facebook checked in with the highest brand value of any social web property at $29.1 billion, with YouTube in second place at $18.1 billion. Assuming a $100 billion market cap for Facebook, and applying Facebook’s brand value to market cap ratio, that pegs YouTube at a $62.2 billion value.

UPDATE: The last paragraph has been edited to input the correct brand value and market cap numbers thanks to Matt in the comments below. Again, more detailed numbers analysis to follow sometime next week.

Elliot TurnerPosted on Monday, March 19, 2012 at 8:27AM

Genomics today is one of those fields where we can witness the Innovator's Dilemma unfold in realtime. I am particularly intrigued by genetic sequencing for a number of reasons. The idea that we are simply complex programs with a coding system that has double the inputs of a binary computer system has major consequences in terms of religion, philosophy, and most visibly, health. This is heavy stuff for a former philosophy major! Further, the "anti-evolutionists" have a big problem with this reality, because it willingly confirms and implies we are of the same fiber as every living substance on Earth, have thus evolved from the Great Apes, and are already developing the capacity to manipulate the structure of our internal code. Can we once again call this "debate" over?

In reality, this is a good, not bad thing! With the understanding of how our most basic system works, we can officially launch into an entirely new era of medical diagnostics and treatment. While medical costs have been soaring in the United States to the tune of a decade and a half of double-digit growth, genomics, once wildly expensive, holds the key to generating enormous cost and treatment efficiencies. With knowledge of an individual's genome, we can came up with better treatments for each individual, skip many of the painfully unnecessary diagnostics, and develop a personalized course of action, all at a lower total cost.

Plus, as an added bonus, we can refine our Pinot Noir grapes to taste as we want it, grow where we want it, how we want it. I'll let Barry Schuler take over from here on what genomics is doing for us today, and what we can expect to see tomorrow (here's the link in case the embed doesn't work):

Elliot Turner Posted on

Elliot Turner Posted on