Elliot TurnerPosted on Monday, April 9, 2012 at 1:24PM

I want to skip over reviewing the device, because its awesomeness has been acknowledged a million times over, with little unique to say. Instead I’d like to jot down some notes on how the iPad 3 has impacted my web browsing and media consumption. Over the course of the past month, there are some notable changes in my long-term habits that I have developed, which I think portend at least a little about the future of technology and media. Please note, none of these points are supposed to be right or wrong, they are simply observations about how my personal habits have changed.

iPad and Video

By far the most impactful shift has been my embrace of web video. I always watched the occasional video, and with my GoogleTV, I started watching a bit more online video content. Now with the iPad, web-based video has chopped my TV viewing time in half, and has eroded a decent chunk of my web reading time allocation as well. In fact, reading has been a far more significant loser since getting the iPad than anticipated. Reading had always been the means through which I pursued my primary interests and my self-enrichment time, while video was primarily my escape time. Even between cable, on demand and DVR, I didn’t have nearly enough video content that was “smart” and crafted for my desires. Now with the iPad it is far simpler than ever before to seek out and consume interesting and informative content that meets my tastes.

Now, I spend about 30 minutes a day watching TED Talks on different rewarding topics, and an additional 30 minutes of select YouTube content, ranging from old interviews, to lectures from some great thinkers, to cool videos of nature. Altogether, I find that the video watching I do on the iPad is distinctly different from what I watch on TV, therefore it has only cut out of my mindless TV time, rather than my entertainment TV time

(Slight digression: to me, mindless and entertaining are distinct types of consumption. Mindless are those channels I put on because there is no other option, just to clear my head, while entertainment is the content that I am thoroughly addicted to seeking out. Mindless TV for me is watching a Seinfeld rerun for the millionth time, while entertainment TV is watching the latest episode of Mad Men).

To that end, the amount of mindless time I spend watching actual TV has shrunk substantially (i.e. watching something just for the hell of it, when there is little else to do, like the 45 minutes while in bed before sleep), and has been replaced predominantly with much smarter content. I feel better for it at the end of the day too. All this helps further confirm my belief that YouTube will be a big winner in the future of video.

iPad and my Computer

One of the biggest changes is on the bigger level, about how I use my computer. My computer has become my exclusive domain for productivity functions, while the iPad, although not monopolizing consumption, has become the primary outlet through which I consume content. It’s just so easy to read and watch on the iPad, while still relatively difficult to coherently build something. I have used it in a complimentary role for my stock research, mostly as a 2nd screen and an easy way to visually see something that I am manipulating in either Excel or Word.

There are two important observations here. First, while the iPad is great for consumption of information, it really isn’t all that good for productivity functions. For this reason, I think all those who fear the imminent demise of the PC are overlooking the obvious—people use computers to both use stuff and to do stuff, and doing stuff isn’t going anywhere anytime soon. For data analysis and writing, the iPad simply cannot compete with a computer, and there is no reason as of yet to make that transition. Second, the iPad is much easier and more efficient for consumption, not because the screen is so shiny and pretty, but because the combination of finger flicks and taps is much simpler, smoother, easier and more fun than a keyboard and track pad, especially when making words out of buttons (aka typing) just is not necessary. The simplicity and fun combined are a powerful force in driving said consumption to the iPad.

The Future

The iPad alone brings cord cutting much closer to reality. One of the real consequences is that quite a bit of my personal cable-watching time has shifted to the web, and that trend will definitely continue to accelerate. With apps for each of the major networks, covering the majority of the shows I actually watch, the only real missing link continues to be live sports. As soon as the day arrives that sports are available for streaming on the web (note to the cable companies: you can only fight the inevitable for so long) my cord will be cut and cable will be in my past.

Elliot TurnerPosted on Tuesday, March 20, 2012 at 3:45PM

Want to invest in one of the best, most innovative startups in the world with taking none of the risk associated with a startup, and more potential upside than many of the most popularly watched private market web names like Facebook? Look no further than the strongest brand hiding behind the Google name: YouTube. YouTube is turning into a huge business, and were it a standalone start-up, the company would easily be one of the most valuable Internet companies and one of the most hyped. Instead we hear little about YouTube’s business other than the obligatory question and non-answer answer on each Google quarterly conference call about when/if/how much money YouTube will make.

Today, YouTube seems even more an afterthought in the narrative about Google the company than Android and Google + and I can’t help but find the irony and humor in it all. While everyone is waiting for Google’s true “social” answer, and even Google itself is out there searching (pun intended), YouTube is in fact a social, technology and media behemoth in its own right. After all, it is the place where “going viral” became the thing to do (speaking of which, here’s a cool video with Kevin Alloca, YouTube’s “trends manager” on what actually makes a video go viral).

Facebook is the startup darling of the world, Netflix at times has been the streaming superstar, and Apple is…well…the apple of everyone’s eye. Meanwhile in between watching hours of YouTube videos a day, everyone forgets that a) YouTube has an amazing business model and b) Google is both cheap and sitting on a competitive Trojan Horse. Let me explain.

The Cost of Content

I’m oversimplifying here, but in content, there are the producers, the distributors and the consumers. When anyone talks about content distribution companies, and video in particular, the cost of content is important in determining the bottom-line profit. The true advantage of streaming video is that on a relatively small fixed cost base, a distributor can reach every web-connected person on Earth. In an ideal world, that sounds like a simple and great business, but the content producers have only been willing to engage the distributors with largely one-sided terms.

The content producers know full well the value in distributing via the Internet, so they even created their own distribution service—Hulu.com. Netflix has used its DVD business, the company’s cash flow machine, in order to fund content acquisition for its streaming service. As streaming has gotten easier and more popular amongst the masses, many have fled DVDs for streaming, thus forcing Netflix to improve its content mix online. As their early contracts expired, the company found itself having to negotiate in a position of need with the studios, and since then has paid a hefty price.

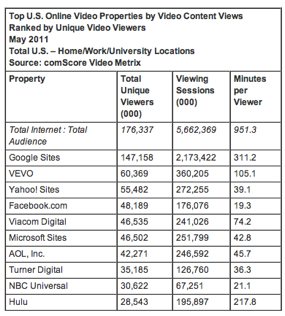

Meanwhile, YouTube just keeps doing its thing. Worldwide, people view 3 billion YouTube videos per day, which for perspective is “the equivalent of nearly half the world’s population watching a YouTube video each day, or every U.S. resident watching at least nine videos a day.” While Netflix and Amazon are out paying (more like begging for the right to pay) for content, YouTube users are willingly uploading 48 hours of content per minute for FREE. Granted not all YouTube content is as desirable as the content others are paying for, but considering how many people watch videos on the site every day, it’s safe to conclude that at every minute YouTube is gaining more valuable content at no expense.

With this recipe, YouTube has become the most watched online video site by a mile (h/t to TechCrunch for the chart):

In the process, YouTube has already become a heavily entrench business with a strong brand name and strong brand loyalty. When people talk about the competition for online video success, particularly in financial circles, the competition pits Netflix against Amazon, with Apple sometimes entering the fray and Google a total afterthought. That needs to stop.

As of today, YouTube has already reached deals with CBS, BBC, Universal Music Group, Sony Music Group, Warner Music Group, the NBA and the Sundance channel, amongst others (contract list from the CrunchBase). Some of these deals were reactionary to growing pressure from content producers at the copyright infringing uploads done by YouTube users, but at the end of the day, these content deals have done a whole lot to enhance the quality of the videos available on YouTube and entrench the site as THE go to platform for video.

Notice a theme with these content deals? Many of the early deals are music-centric. There is no better place on the Web to watch high quality concert video than YouTube, nor is there a better place for an artist to debut their new song via a video (even VEVO uses YouTube), with MTV now a soap-opera-type channel lacking any coherent connection to music. Witness Cee-lo Green’s catchy release of F*ck You with the words literally dancing across a blue projection screen. This was both a powerful and catchy way for Cee-lo to get his song out to the masses, and was a catalyst behind the song’s ascent on the pop charts.

YouTube the Platform

The Cee-lo release provides the perfect segue to YouTube as a platform. YouTube is a disruptive medium in itself, but more interestingly it has become a platform upon which other disruptions are launched. At the same time, YouTube has also become a video platform that is ubiquitous across all viewing platforms. Although a web-page in itself, YouTube is a “channel” (rather app, but what’s the difference these days?) on any web-enabled TV device from designated viewing devices like the Roku or AppleTV to gaming systems like the Xbox. The point is that YouTube has both incredible reach to its audience, and is an innovative vehicle for some of the world’s foremost innovators. Even Apple can’t deny this reality.

In addition to debuting singles on YouTube, there are successful artists who owe their entire careers to the medium. Look no farther than Justin Bieber (geez I promised myself that name would never be typed into this blog…), someone who would never have been “found” had it not been for the site. Bieber isn’t alone. Daniel Tosh has built an incredibly popular show on Comedy Central based entirely off of YouTube videos, and the Young Turks have become serious news pundits from their YouTube show.

Louis CK, a comedian with a strong cult following, used YouTube in an entirely new way by releasing his “Live at the Beacon” directly through the platform. “Lucky” Louis went on to sell this show for $5, with customers able to pay and watch instantly. This is far cheaper than a DVD retails for, and a much easier way to directly connect with an audience. The move was both highly profitable for Louis, and rewarding for his fan base.

When you have a business that works better for all the parties directly involved than the existing business model, you have a powerful force. It’s cheaper for fans, more profitable for the artist, reaches a far wider audience than anything else, and has fewer intermediaries taking a cut. Stuck in the middle is YouTube/Google easily (and happily) collecting its margin. It’s only a matter of time before more artists follow Louis down this path.

And YouTube’s appeal isn’t limited to music, comedy and entertainment. The Khan Academy is using YouTube as platform to disrupt education. While it is a non-profit that produces free, high quality educational content for view via the YouTube platform, let’s not dismiss the fact that the Khan Academy is proving the power of the platform as a way to not only reach those interested in learning, but to fundamentally change the way eager students learn. TED Talks has also used YouTube in a similar manner as a platform to bring informative, educational videos to the masses. We’re only just beginning.

YouTube and the Innovator’s Dilemma

YouTube is following the path of the Innovator’s Dilemma, and all of the dominant market leaders in the sectors impacted by the company are already on high alert (if you haven’t already done so, go read the book now, or for a short-cut read my blog post on it). YouTube has firmly entrenched itself on the low-end of the video-watching marketplace, and I mean this both in terms of Internet video, and video in the broadest possible terms. Further, YouTube has significantly deflated the cost of distribution and consumption, making both effectively free in many contexts for the content producer and the viewer respectively. In doing so, YouTube generates a fairly high margin on its advertising dollars on.

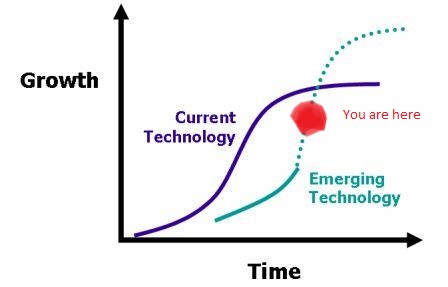

As YouTube has earned more and more money on the “low hanging fruit” (aka the free stuff) they have been able to step up their acquisition of premium, higher quality content. Some of the aforementioned deals are evidence of this. In other words, the company is using its entry level product, which has helped it gain market share, in order to fund its climb higher up the distribution tree. As a result, the company is in the midst of a further pivot up its S-curve (H/T to Your Brand is Showing for the graph).

The current technology is the combination of TV/Cable/Internet that we presently view video on, while the emerging technology is YouTube. In my imprecise opinion, right now YouTube is somewhere around the big red dot that I drew on top of the chart. The company is on its parabolic ascent, but has yet to reach and cross the current technology in its prowess, largely due to the defensive posturing of the existing infrastructure. But that can’t last forever. As the chart indicates, and as is typical with disruptive innovation, YouTube’s day is coming rather quickly. Keep in mind we’re talking about a company and technology barely more than six years old. It was within the past two years that we were introduced to high definition video for streaming, that we were able to watch YouTube video’s on our television, and even more recently, that content was divided into organized channels.

Not long ago, YouTube had a major success in acquiring streaming rights to a premier Indian cricket tournament for live games. Viewership surged far quicker than anticipated, and was more profitable than anyone expected. Soon many of the major sports leagues will have their television contracts expiring, and one can imagine that YouTube will be a player for the rights, especially considering their already strong relationship with leagues like the NBA and NHL. If YouTube were in fact the first to bring mass-streaming of live sporting events to the American masses, they would be the first to truly liberate video viewing from the existing infrastructure and into the digital age. After all, live sports viewership is probably the single largest impediment to would-be chord cutters today (myself included).

YouTube gets this, as is evidenced by what CEO Salar Kamangar recently had to say: (h/t to New Markets Advisors, I strongly recommend reading their write-up on the disruptive power of YouTube as well):

"When you think about the impact cable had, we think we're in a position to have a similar impact for video delivery, like what cable has done with broadcast. In the early '80s, you had three or four networks. Now those three or four networks are responsible for 25 percent of viewership, and the cable networks are responsible for all the rest. Right now, the fraction of traffic that is Web video is small relative to broadcast and cable, but it's growing at a fast rate. What's amazing is that the Web enables you to build a kind of channel that wouldn't have made sense for cable, in the same way cable enabled you to build content that wouldn't have made sense for broadcast. You couldn't have done CNN with the broadcast networks; you couldn't have done MTV with the broadcast networks."

And here’s a great TED talk with Chris Anderson, Editor in Chief of Wired Magazine, on “How YouTube is Driving Innovation”: (obviously an embedded YouTube video)

Putting the Story in Context with the Numbers

Now that I have established a benchmark for how awesome and disruptive YouTube is, the next step is to take a look at the number. If you’ll remember, my initial premise was that one can buy one of the most disruptive, innovative companies today without taking any of the venture capital risk, for free. This requires that I establish two premises: 1) that Google without YouTube is at most, fairly priced, if not downright cheap, and 2) that YouTube as a stand-alone entity would be worth a sum exceeding $10 billion in market cap, and in a range that reaches northward of $20 billion. For that I will have to follow-up with a second post, but I will not leave just yet before beginning the next step of the argument.

Using consensus analyst estimates on revenue for 2012 (courtesy of Business Week), a 10% WACC and 4% perpetual growth, Google has an earnings power value plus growth of $680, that is a 7% premium to this price. YouTube itself accounts for a mere 4% of Google’s in this estimate, and if you removed YouTube’s revenue contribution entirely from Google, the price drops to $653, a 3% premium to today’s price. From this, we can deduce that YouTube represents about $27 per each share of Google, or a total intrinsic value of $8.7 billion.

Before next week’s post on how to value YouTube, I just want to finish off by stating my belief that $8.7 billion is way too cheap for such a valuable web property, especially when companies with lower revenues like LinkedIn and Zynga are trading for near $10 billion, and Facebook is pricing at over $100 billion. In a recent social brand value analysis by BV4, a brand value ratings agency, Facebook checked in with the highest brand value of any social web property at $29.1 billion, with YouTube in second place at $18.1 billion. Assuming a $100 billion market cap for Facebook, and applying Facebook’s brand value to market cap ratio, that pegs YouTube at a $62.2 billion value.

UPDATE: The last paragraph has been edited to input the correct brand value and market cap numbers thanks to Matt in the comments below. Again, more detailed numbers analysis to follow sometime next week.

Elliot Turner Posted on

Elliot Turner Posted on