Last week, in addition to attending in person the Santa Fe Institute conference, I also “virtually attended” the European Investing Summit put on by ValueConferences and the Manual of Ideas. It too was quite the experience, in terms of the quality and quantity of content and its groundbreaking format for connecting global value investors. These days it’s nearly impossible to amass the brainpower and experience of informed presenters in one conference room over the course of two days in any physical sense. That’s why the Manual of Ideas had the idea to orchestrate a virtual conference, with a blend of live streaming and pre-filmed interviews, replete with presentations and interactive conference rooms to connect with fellow attendees and presenters alike. Many thanks to John and Oliver Mihaljevic for conceiving and executing on an outstanding idea, and for gathering some of the foremost talent in the industry.

I spent a whole lot of time last week and over the weekend listening to and absorbing as much as I could from the videos. I particularly liked the fact that nearly all of the videos offered great lessons on the process and philosophy side as much as they did on the ideas front. I went into the conference with plenty of thoughts on Europe and where I saw the crisis inevitably leading to, plus I had already deployed capital strategically into four distinct European investment opportunities, but I really wanted more considering the vastness of opportunity amidst crisis. (Be sure to check out my post connecting Europe today to the Articles of Confederation USA entitled The Answer to the Eurozone Crisis was Written in 1787).

I “left” the conference having learned of several very intriguing ideas that are queued up for immediate further inquiry, but maybe even more importantly, I “left” feeling like I made important strides in continuing the evolution of my own investment philosophy. In this blog post, I would like to share some of the more macro ideas from the live sessions on day 1 of the conference, including perspectives on the European markets and some important philosophical points on value investing in this present environment. Anyone who finds these ideas remotely intriguing would extract considerable value from attending these online sessions at ValueConferences.com.

Guy Spier, Managing Partner, Aquamarine Capital

The live portion of the event kicked off with Guy Spier’s keynote address on “Investing in Europe in the Face of Crisis and Uncertainty.” Spier started his analysis with some very informative charts on the debt-to-GDP ratios of the various EU entities, including a breakdown between public, private and corporate debt. There were some interesting observations on the charts, including just how troubled Greece is from a public debt perspective, how much greater Ireland’s aggregate debt burden is compared to the rest of the EU and US, and how much actual private wealth exists in Italy. Obviously we all know about Greece’s woes, but I think in valuing investing circles, the troubles of Ireland stand in stark contrast to conventional wisdom, and Italy’s wealth is often overlooked (this is something I’ve covered on my blog in the past in a post called Why Italy Doesn't Worry Me).

In my opinion, one of the more important points Spier made off of these charts is that “fear-mongers try to make money off of selling fear, but the globe has a whole lot more wealth than is ever talked about.” This is exactly how crises go. People get caught up in the negative emotion and willfully look past some crucial realities.

We then turned to a chart on the odds of a country leaving the EU, which has greatly decreased since ECB President Mario Draghi’s aggressive late summer statements and actions. This segued nicely into how Guy in the recent past thought the Euro would in fact break up, however, politics, not economics paved the way for Draghi to bypass the rules in practice, and keep the currency union together.

Next Spier broke down the two lenses through which people view this crisis: the Anglo Saxon vs. the Continental. Anglo Saxon countries are more individualistic and place a greater degree of value on personal freedom, whereas the Continental lens is more collectivist. This creates a dichotomy whereby those who adopt the Anglo Saxon perspective view the crisis through an economic lens, while Continental people take the political view. Each perspective has its own unique consequences; however, it’s clear that today the Continental approach is winning.

Spier himself asserted that he has moved his understanding in the Continental direction. This then evolved into a discussion on how the crisis itself is a catalyst for further integration to the point where without crisis, integration itself stagnates. That raises the question of whether crisis is desired amongst those integrationists like Draghi, for without it they cannot continue the mission of Jean Monnet.

Please note: Spier then gave some very interesting investment ideas, but again, my focus here is to outline the European perspectives and what I learned philosophically about value investing.

Charles De Vaulx, Chief Investment Officer and Portfolio Manager, International Value Advisers

Right off the bat, De Vaulx continued on this theme of an Anglo Saxon/Continental divide: “Investing has always been an Anglo Saxon endeavor…it’s mostly those countries that have relied on capital markets to advance capital formation, while other countries saw their capital formation financed in other ways.” De Vaulx then launched into a great history of value investing, and how it had predominantly been an American, and then British phenomenon. Starting with the early 1990s recession, great American investors like Tweedy Brown and Michael Price ventured into global capital markets for value, mainly Europe.

Why did these investors turn to Europe? De Vaulx argues that this is due to some of the competitive advantages offered by European reporting. Before the adoption of international account standards in Europe, man companies made it easier for some equities to get mispriced, or they ended up undervalued due to very conservative accounting practices (the opposite of many other places in the world). In many of these cases, true economic earnings were thus understated. Likewise, many companies had hidden assets on their balance sheets that were booked at historical cost, rather than present value.

Previously, the abundance of family owned and controlled businesses had been thought of as a risk in Europe, yet on further analysis, it became clear that these families were true stewards of investor capital, with their risks aligned in an advantageous way. Further, many were open to the idea of takeovers and/or mergers as a means through which to realize value.

Right now, International Value Advisers has 10% of the fund invested in France and only 0.4% in Germany. This sits in contrast to much conventional wisdom, which holds that Germany is the safest, and France’s regime will crush capitalism. Many companies across Europe, and particularly in France are in actuality global businesses, with a plurality of income generated overseas (De Vaulx used Vivendi and Total as examples here).

Over the course of the Euro Crisis there has been a big distinction in stock performance between the quality businesses and the cyclical ones. Right now, many of the high quality businesses have performed very well, and thus are not cheap, while the cyclical businesses have become increasingly depressed. Because of this contrast in performance, De Vaulx has been selling some quality businesses and allocating more capital towards the cyclical ones. Because of this dichotomy, if you look at Europe in aggregate, the markets look very cheap; however if you want to buy quality you have to be willing to pay up.

Interestingly, De Vaulx had two impactful statements which contrast with typical value investing theory: first, he said that “gold has a lot to do with value investing and has a lot to do with Europe” as a hedge against problems; and second, he said that “buy and hold should not be part of the value investor’s vocabulary right now” due to the heightened volatility, which will be with us for a while. This is an interesting adaptive change for a long-time value investor.

Alvaro Guzman de Lazaro Mateos, Managing Partner and Portfolio Manager, Bestinver

Bestinver is a long only, no derivatives value investing group that follows macro, but doesn’t invest it. Guzman de Lazaro focuses much attention on the reasons why a security has become cheap, and when an answer is readily identifiable, he invests so long as the reason for cheapness are acceptable. In Europe, much of their attention is focus on family owned companies, companies with weird share structures, long-term projects and under-the-radar small caps.

Guzman de Lazaro observed that by and large, “Europe is a less efficient market” and in my opinion, this is music to any value investor’s ears. For without inefficiency, there cannot be value, and the greater the degree of inefficiency, the greater the opportunity. Guzman de Lazaro continued that in the US there is far more competition amongst the various value investors, and competition drives down return. With European family owned businesses, there is a unique opportunity to engage with the families in order to develop a synergistic relationship over the course of years. These families start to see their big investors as partners, and take their input in capital management.

Typically, Bestinver will look for companies with high barriers to entry, trustworthy management, little or no debt, and the stock already down quite a bit, all the while value itself should be growing. What they prefer is a stock to drop solely due to concerns about the European Union itself, and not the fundamentals of the business. Guzman de Lazaro emphasized the importance to their margin of safety of the increasing of intrinsic value while the price either stagnates or drops lower. This creates a situation where over time the company has gotten cheaper. Because a breakup of the EU cannot be taken off the table, Guzman de Lazaro models each company accounting for a 40% devaluation in their respective domestic businesses.

Guzman de Lazaro also presented two excellent ideas, one of which is now on my immediate research list, and I urge you all to check out the European Investing Summit to learn more.

Jochen Wermuth, CIO and Managing Partner, Wermuth Asset Management

Jochen Wermuth is an investor focused on Russia and his presentation was appropriately titled, Russia: Klondike or Eldorado? I went into the presentation disliking Russia and wanting to dislike it more. Everything we hear about the country is of government and corporate corruption alike, with a near dictatorial leader imposing his well as he sees fit. While there is certainly much merit to these complaints, Benjamin Graham certainly would still invest in a cigar butt were the valuation cheap enough, with little regard to the quality of the business itself. And it does seem like Russia has some impressive numbers working in its favor, and we’re talking verifiable, not corruptly skewed numbers here too.

Wermuth started with the assertion that valuations are extremely depressed, and the reasons are twofold: the perception issues cited above, and a dose of truth. The government has been increasing its share in the economy, and extracted significant value from the oil sector in order to build a substantial sovereign wealth fund. To that end, there have been rollbacks in the pace of privatizations, and more dangerously, people in the country have been deeply upset by corruption to the point where they want to leave. As a result, the country’s equity risk premium now sits at 17%--all-time highs, and a 36% discount to its average PE over time, and a 58% discount to the rest of the BRICs.

That starts us on the good stuff—the country is priced for the worst case scenario. Importantly, government debt, as it stands right now, is at 10% of GDP and the country has zero debt denominated in foreign currencies. This is in stark contrast to many other countries around the globe. Plus, Russia has $520 billion of its own FX reserves, the 3rd largest stash on the planet. This is a very different Russia than the one which defaulted in 1998.

As it stands right now, market infrastructure is not very developed, with foreign capital the primary “bid.” Pensions in Russia are small and cannot invest in equities, therefore the market really just moves along with the flow of international capital. When the tide rides in, valuations rise, and when it leaves, they decline. Further, speculative flows focus on only a few sectors (i.e. the love for emerging market consumers) to the point where there are substantial valuation gaps between the sectors. Liquidity (or the lack thereof) compounds these problems, are brokers only push their international clientele into the most liquid vehicles, not the cheapest, best investments.

John Gilbert, Chief Investment Officer, General Re-NEAM

Although this was dubbed the European Investing Summit, John Gilbert focused his really thorough presentation on the present state of the US economy and its implications for long-term investors. Gilbert posted some outstanding charts highlighting the state of the economy today and how it has changed over time. One of the first observations was that both household net-worth to disposable income and household net worth to debt have both improved since the crisis began, albeit not very much overall. Plus the savings right, while higher now, has to potential to get even more elevated.

Financial sector debt-to-GDP has risen from “virtually zero” in 1952 to a peak of 120% of GDP in the bubble days, back down to about 90% now. Deleveraging has been particularly rapid in this sector of the economy, but it “may have considerably further to go.” Leverage in the shadow banking arena (mortgages, ABS and other) is greater than in the traditional financial sector now, and this can be attributed to the financialization of the economy.

Gilbert then asked rhetorically, “how far along are we on deleveraging, and how much further do we have to go?” In 2011, the Bank of International Settlements presented a paper at Jackson Hole called the “Real Effects of Debt.” The BIS outlined how in each of the 3 sectors, levels of 85-90% of GDP correlate to slower subsequent economic growth. We are still in this danger zone.

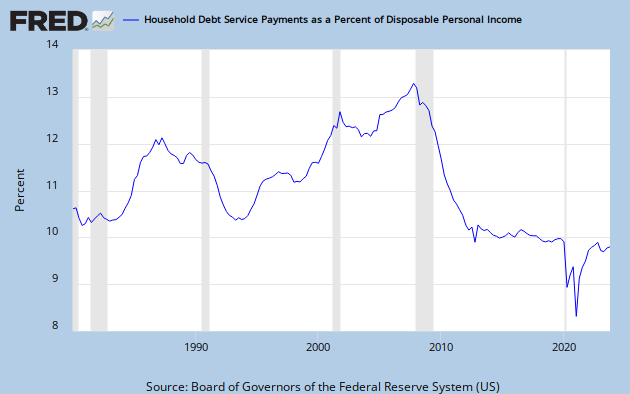

Many optimists point to the debt service as a percent of disposable income in order to say thing are getting better, and the Fed does this too (for my Twitter followers, you know I’m guilty as charged here too…see the chart for yourself here). Gilbert says “it is quite encouraging” and certainly has some merit, and says the reasons behind this are the Fed’s zero interest rate policy (ZIRP) and what that has done to create low mortgage interest rates. However, Gilbert would caution that the balance sheet itself remains quite stressed and this leaves the household sector vulnerable to any subsequent shocks.

Historically, the largest source of deleveraging has been from increases in nominal GDP, most specifically inflation. While there are no imminent signs of inflation, this is a good template through which to expect future deleveraging to take place and its worth looking at where inflation might come from. Plus, the aid of inflation in decreasing debt burdens can be quite large even when the overall inflation rate is low. Policymakers are aware of this, but there problem is that it’s tough to get inflation started in the short run.

Housing is typically a good source of inflation, although it “won’t surge anytime soon.” It is clearly off the bottom today, and we’re heading in the right direction. Single family rental rates (or the bond equivalent value of owning a home) has diverged sharply from the price of actually owning a home. This makes renting more expensive relative to housing and pushes would be renters into homeownership. This is a good positive for housing.

As for Fed policy, QE3 is different from its predecessors both in terms of conditions in advance (they’re a bit better now) and in the way it’s done (open-ended purchases of MBS instead of fixed amounts of Treasuries). This marks an important “cultural change in the Fed” that is moving towards unanimity in the dovish direction. We can see this in how certain members have changed their positions to align with Chairman Ben Bernanke. Since QE3 is tied with the Fed’s goal of “maximum employment” we must then examine what that term means. Gilbert defines it as “the rate when the economy is at potential and not exerting pressure on inflation.” The problem is that this rate shifts over time, and is not observable. It therefore “must be inferred from the condition of the labor market.”

One way that policymakers try to figure out “maximum employment” is through using the Beveridge Curve. This plots the unemployment rate against the job opening rate. There are two problems with this analysis: the natural employment rate is subject to error, and there is a big spread between the real-time data and revisions down the road. Right now it’s too early to form any strong opinions about the labor market, as to whether there has or has not been structural change in the economy. The Fed is inclined to say there is not; however, Gilbert is a bit more skeptical and wants to wait to make any judgments.

Everyone today is looking for more yield, but it’s important to remember that these are troubled times and more yield involves more risk. We are approaching tight corporate bond spreads on high quality stuff, but not quite yet on high yield. There are many anomalies in markets due to this chase for yield, including: electric utilities trading at their highest P/E relative to the S&P ever, the Schiller CAPE/Tobin Q are not all that cheap right now; Gold has outperformed the S&P despite not being a good long-term investment in its own right. Gilbert elaborated on gold saying that once in a while it acquires option value, but doesn’t pay off very often. It is “only in the money when people lose faith in the existing monetary standard” and considering that faith has not broken, gold “is a candidate for a bubble.”

In conclusion, Gilbert explained that it’s too early to say whether there has been a permanent behavior change following the recent crisis, but it’s significant that most people alive today have never seen anything other than credit inflation. Lehman itself upended 200 years of lender of last resort behavior, and this in and of itself could have far- reaching consequences down the road, leading people to take on less debt for a long time, and/or possibly inducing central banks to be more aggressive than they have been.

I had the opportunity to ask a question, and I asked: “you referenced the connection of maximum employment to NGDP and the Fed’s new form of QE2 as a more forceful push towards maximum employment. Do you then view QE3 to be the fed’s adoption of NGDP targeting?” Gilbert answered that it’s not quite there, because there are technical problems with targeting NGDP. He does however expect the idea of NGDP targeting to get more attention, because it would allow the Fed to let inflation rise without actually saying so.

Gilbert continued to explain that If we end up in a world where the US is not a real growth economy, but a 2% real GDP growth state, and you set an NGDP target of 5%, this lets your target inflation rate rise from 2% to 3% without actually doing anything. Further, he said that it’s hard to see QE3 having the transmission mechanism to support such a substantial change in their targeting. They’re solely resorting to increase the quantity of money right now, rather than the cost of money, which is what NGDP would do. For that reason, the Fed might have to take more radical steps were they to actually adopt NGDP targeting as its policy.

Elliot Turner Posted on

Elliot Turner Posted on

{kind=link}

The Psychology of Markets at All-Time Highs

Here is our latest market commentary from RGA Investment Advisors, taking a look at the psychology of markets trading at all-time highs. This is an interesting moment, for it is the first time in my professional investment career that markets are in fact at highs. This is our attempt to put things into perspective:

The Market at an All-Time High

Last month, we pointed out the significance of all the major market indices (sans the NASDAQ) surging to record highs. April was an interesting month in a very different way. While the major indices digested their gains, there was absolute carnage in the commodity space. Most notably, gold, the safe-haven of choice for investors over these last few tumultuous years, shed 7.57% on the month. In one day alone, gold lost 9.6% of its value. Many continue to blame the decline in gold on some sinister plot or dismiss it as a warning sign for the broader economy. We think these explanations are far more indicative of the “religion” around gold as an asset, than it is of something meaningful for the economy; we discussed this in our February 2013 Investment Commentary. To that end, we attribute the decline in gold to two important forces: 1) gold’s failure as a safe-haven during the worst of the Euro crisis, during which the price actually declined; and, 2) the market’s continued resilience at all-time high levels. Today, we would like to focus on this second point and what it means for the broader investment environment.

First, a necessary digression: we are pleased to say this is the first time in the history of RGA Investment Advisors with the U.S. stock market in milestone, record high territory. This company was founded amidst the biggest financial crisis since the Great Depression and we take pride in how we have navigated through what even the most experienced sages of market wisdom declare as one of the least forgiving, most challenging investment environments ever. We promise both to you and ourselves that these years will serve as an important lesson in patience, strategy and humility, for we all know that while today the market giveth, it can just as easily taketh away.

We are self-reflexive at this moment because we think it’s important to be cognizant of the many emotions induced by the market over time. Further, we constantly want to learn more about how and why the market does what it does from a behavioral perspective, and to that end, have studied the great thinkers in that arena. One particularly intriguing school of thought is Prospect Theory, which we have introduced in commentaries past. Investopedia defines prospect theory as “A theory that people value gains and losses differently and, as such, will base decisions on perceived gains rather than perceived losses. Thus, if a person were given two equal choices, one expressed in terms of possible gains and the other in possible losses, people would choose the former.”[1] To that end, it is the study of how people make probabilistic decisions when there is a degree of both risk and reward, and it holds that people are more sensitive to losses than they are to gains. In other words, the pain from losses leaves a more profound impact on the human psyche than the pleasure derived from gains. This idea was introduced by Daniel Kahneman and Amos Tversky in 1979 in a paper entitled Prospect Theory: An Analysis of Decision Under Risk[2] and has been expanded upon ever since.

A corollary of Prospect Theory is an idea known as “the disposition effect.” This idea holds that people sell stocks that have gone up far quicker than stocks that have gone down. The disposition effect is closely tied to the concept of “myopic loss aversion” covered in our January 2013 commentary. Why are these ideas relevant today? Interestingly, the disposition effect has particularly strong consequences with markets in all-time high territory, and we feel it is important to review them in light of today’s investment environment. Since people sell gains quicker than they do losses, there is a greater propensity for selling above all-time highs than below. Therefore, when markets are at all-time highs, selling pressure tends to increase, leading to greater portfolio turnover in Bull than Bear markets.[3]

Drawing this out further is the important idea that loss aversion does not exist in a vacuum, and as such, there is a reflexive relationship between the success (or lack thereof) of prior decisions and the nature of present and future decisions to be made. For the typical investor, “after prior gains, he becomes less loss averse.”[4] In other words, people are most risk-seeking after periods of success and most risk-averse after periods of failure. Meanwhile, prudence would dictate practicing the converse. This pendulum of risk tolerance fluctuates back and forth dependent on the most recent market action. Collectively, these ideas relate to another concept we have long discussed—the notion that people fear a crisis most in its aftermath, rather than its inception. It is thus no surprise that some of the biggest doomsayers in today’s press are those who were caught most off-guard by the crisis in 2007-2009.

So where do we stand today on this sliding scale of risk aversion? We think it remains clear that investors have been severely impacted by the recent crisis. Investors are so risk averse in today’s environment, that in aggregate, they would rather flee into the perceived safety and certainty of returns in bond markets, while simultaneously ignoring longer-term bond market risks and foregoing a more reasonable tradeoff between risk and reward in equity markets. Despite markets making all-time highs, there remains a healthy skepticism, and even anger, at the very fact this is happening amidst what remains an economy performing closer to trough than peak levels.

As always, we continue to make our decisions based on our sensitivity to price in each and every individual investment that we make, though we are equally cognizant of the sentiment towards risk and reward around us. When markets are making highs, so many want to be “the one who called the market top” yet we can assure you of only this—on the way up there will be many tops before there is THE top, and it is our belief that through prudent bottoms-up fundamental analysis and disciplined asset allocation we will best insulate ourselves from the type of risks that were borne out in 2007-09.

Past performance is not necessarily indicative of future results. The views expressed above are those of RGA Investment Advisors LLC (RGA). These views are subject to change at any time based on market and other conditions, and RGA disclaims any responsibility to update such views. Past performance is no guarantee of future results. No forecasts can be guaranteed. These views may not be relied upon as investment advice. The investment process may change over time. The characteristics set forth above are intended as a general illustration of some of the criteria the team considers in selecting securities for the portfolio. Not all investments meet such criteria. In the event that a recommendation for the purchase or sale of any security is presented herein, RGA shall furnish to any person upon request a tabular presentation of: (i) The total number of shares or other units of the security held by RGA or its investment adviser representatives for its own account or for the account of officers, directors, trustees, partners or affiliates of RGA or for discretionary accounts of RGA or its investment adviser representatives, as maintained for clients. (ii) The price or price range at which the securities listed in item (i) were purchased. (iii) The date or range of dates during which the securities listed in response to item (i) were purchased.

[1] http://www.investopedia.com/terms/p/prospecttheory.asp

[2] http://www.jstor.org/discover/10.2307/1914185?uid=3739808&uid=2&uid=4&uid=3739256&sid=21102235131477

[3] Notes from Nicholas Barberis at Sante Fe Institute’s Risk: The Human Factor conference. http://compoundingmyinterests.com/compounding-the-blog/?currentPage=2

[4] http://forum.johnson.cornell.edu/faculty/huang/prospect.pdf